4 Ways to Reduce Capital Gains Tax

Sure, nobody likes to pay taxes—and capital gains taxes are no exception. But think of it this way: you were smart (or lucky) enough to make the right investment decisions and now you get to cash in on the appreciation.

Although those gains will also come with a tax bill, fortunately, there are steps you can take to legally minimize your tax liability. Here are four tips to keep the IRS from taking a big bite out of your capital gains.

1. Wait a Little Longer to Sell

Timing the sale of your investments is critical to lowering your capital gains taxes. Selling your shares after holding for less than a year will result in a short-term capital gains tax. This means that all the gains you made from the sale of the stock will be taxed at your ordinary income rate, which can be 32%-37% for high-earners. Holding on to an asset for more than one year will be taxed at the long-term capital gains tax rate, which can be 0%, 15%, or 20%.

Holding periods are also critical when it comes to the sale of real estate. If you sell your primary home and you lived in the home for at least two years of the five-year period before the sale, the IRS allows you to exclude the first $250,000 of capital gains (or $500,000 for a married couple filing jointly). While the capital gains exclusions do not apply to investment properties, you may be able to utilize like-kind exchanges to defer capital gains tax by reinvesting in other real estate.

2. Utilize Tax-Loss Harvesting (TLH)

Losing money on your investments is usually a bad thing, but utilizing a tax-loss harvesting strategy means you can claim capital losses to offset your capital gains. If you show a net capital loss, you can use the loss to reduce your ordinary income by up to $3,000 (or $1,500 if you are married and filing separately). Losses above the IRS limit can be carried over to future years. Sometimes it is advantageous to sell depreciated assets for this reason. A tax-loss harvesting strategy can help minimize your tax liability and keep more money in your pocket. However, trying to reduce taxes shouldn’t come at the expense of maintaining a thoughtful asset allocation in your portfolio.

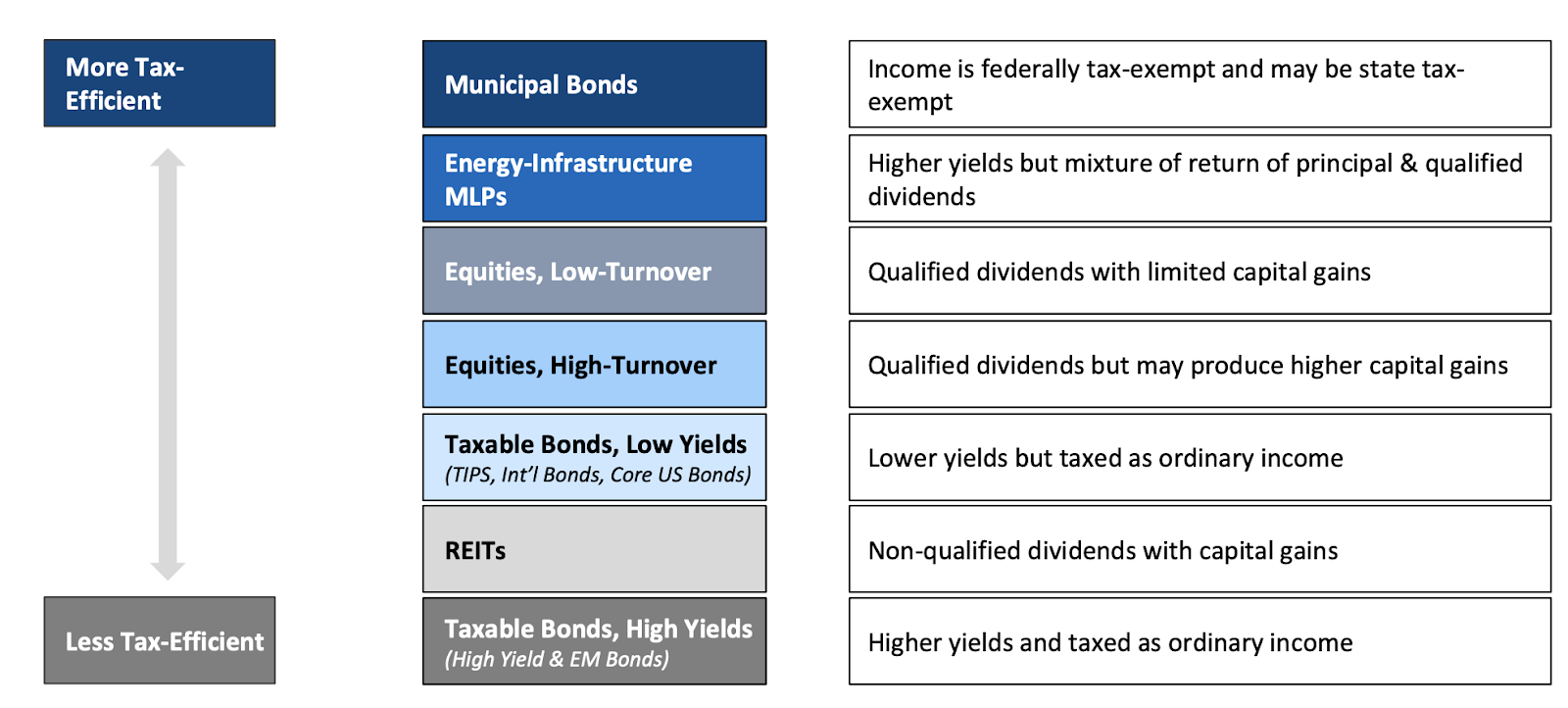

3. Consider Tax Efficiency of Funds Held in a Taxable Account

Some investments will be more tax-efficient than others, as illustrated by the chart below. For example, equities with low turnover will be more tax-efficient than equities with high turnover because there is less potential for capital gains. Active equities will translate into more capital gain income than passive equities, so holding an active investment in your taxable account could cost you tax dollars when you did not make a trade or take dollars out of the investment account. If you have noticed that you have large capital gain distributions and you didn’t sell anything in your taxable investment account, you likely have actively managed funds and it might make sense to look for passively managed funds to reduce your tax liability.

4. Understand Cost Basis & Share Lots

When you buy any amount of stock, the stock is assigned a lot number regardless of the number of shares. If you have made multiple purchases of the same stock, each purchase is assigned to a different lot number with a different cost basis (determined by the price at the time of each purchase). Consequently, each lot will have appreciated or depreciated in different amounts. Some brokerage accounts use first in, first out (FIFO) by default. If you utilize FIFO, your oldest lots will be sold first. Sometimes FIFO makes sense, but not always. Sometimes it is ideal to sell lots with the highest cost basis, which is commonly done as part of a tax-loss harvesting strategy.

Passing on assets as an inheritance can also increase your cost basis. Assets passed on to the next generation at the time of death allow your heirs to pay tax only on capital gains that occur after they inherit your property, through a one-time “step up in basis.” For example, when one spouse dies, assets passed on to the surviving spouse will have a cost basis of the price of the asset on the day in which they passed. This eliminates the deceased spouse’s portion of capital gains.

We’re Here to Help

There are many facets to your overall financial well-being; minimizing capital gains taxes is just one component. Keep in mind that having to pay capital gains taxes is a positive sign that your investment strategies are doing well. Partnering with a financial professional can help you create a holistic plan that is optimized to reach your financial goals.

At Rosemeyer Management Group, it’s our goal to help you build a customized road map for your finances so you can look forward to a comfortable retirement and decrease financial worry. Schedule an introductory appointment online or by calling us at 608-348-2274. For any questions, feel free to reach out to me at kaley@rosemeyermg.com.

About Kaley

Kaley Bockhop is an investment advisor representative at Rosemeyer Management Group, an SEC Registered Investment Advisor based in Platteville, WI. Kaley’s experience in taxes and accounting and her financial planning expertise allows her to help her clients work toward their retirement goals and set themselves up for success. It is Kaley’s goal to partner with her clients to build a customized road map for their finances so they can look forward to a comfortable retirement and decrease financial worry. Kaley is a CPA and a CERTIFIED FINANCIAL PLANNER™ professional. She has a bachelor’s degree in science from the University of Wisconsin-Platteville with a triple major in accounting, agricultural business, and animal science, and a minor in biology. In her free time, Kaley enjoys working on her family’s farm where they raise nationally recognized registered Angus show cattle. She also loves exercising and traveling. To learn more about Kaley, connect with her on LinkedIn.